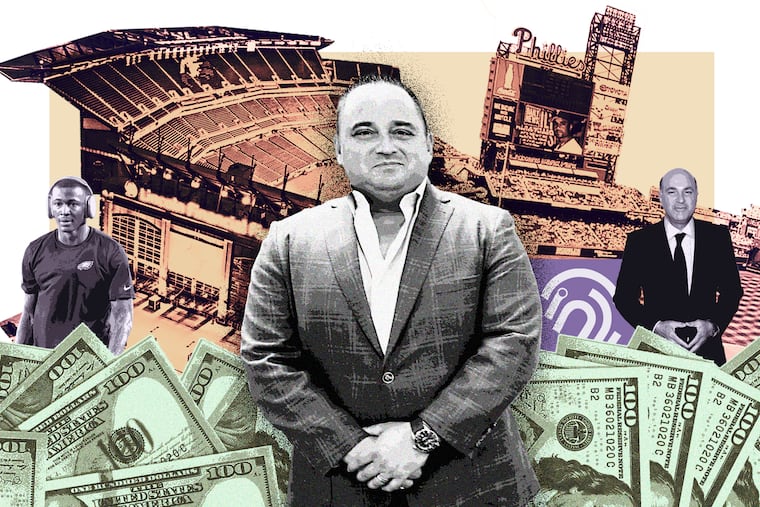

From VIP suites to fraud allegations: A Delco gym manager built an AI-fueled start-up around cancel culture and sports, then fumbled it away

Investors say T.J. Colaiezzi squandered their money on a stadium-sized marketing blitz, hired unqualified friends at inflated salaries, and pocketed a $6 million “bonus.”

Nothing about T.J. Colaiezzi screamed “tech CEO.” He was a former gym manager from Delaware County who had dropped out of college and could not write code. But with $27 million in venture capital in the bank, his AI-powered start-up took a risky marketing gamble in the South Philly stadium complex that announced his big ambitions.

Over three seasons, with the Phillies slugging their way to a World Series, the Eagles racing to another Super Bowl, and a Sixer winning MVP, hometown crowds looked up at scoreboards with ads for his little-known company, LifeBrand. And as Colaiezzi wooed investors from the VIP suites, he sold an underdog story fit for the Philly fanbase and the broader cultural moment.

LifeBrand, he said, was a safeguard for the cancel culture era, with software that could scour years of social media in seconds and flag compromising posts. Users could purge past mistakes with a click and potential employers could avoid making a hire that might later prove embarrassing. Colaiezzi secured support from sports icons like Phillies legend Jimmy Rollins, as well as current and former Eagles.

“Catch all your cringeworthy social media posts with LifeBrand,” Eagles wide receiver DeVonta Smith said in a LifeBrand commercial that showed a photo of a “#wasted” tailgater posted carelessly online.

Now Colaiezzi, 45, is facing accusations of fraud that no artificial intelligence tool can erase.

Hundreds of pages of court documents and internal company records reviewed by The Inquirer, as well as interviews with a dozen people involved with LifeBrand, tell the story of how a fledgling CEO won over deep-pocketed athletes and business owners, and then — following a series of admitted missteps and alleged misspending — was forced to sell the tech company once valued at $137 million for next to nothing.

In two lawsuits, including one filed last month in Delaware Chancery Court, investors say Colaiezzi squandered their money on a stadium-sized marketing blitz, hired unqualified friends at inflated salaries, and pocketed $6 million to finance a lavish lifestyle, including a $4.8 million home in Ocean City, N.J., and a powerboat. Both lawsuits allege that a prominent regional bank and an enthusiastic securities broker helped facilitate Colaiezzi’s deception.

Federal regulators are showing interest in the case, with the U.S. Securities and Exchange Commission (SEC) questioning at least one LifeBrand investor in March, according to correspondence reviewed by The Inquirer. An SEC spokesperson declined to comment.

Meanwhile, the Eagles, Phillies, and Sixers claim LifeBrand owes them a combined $6.2 million in unpaid marketing bills, court records show. And some LifeBrand employees are still owed paychecks from before the company’s collapse.

To the financiers who sued him, LifeBrand amounted to a “Ponzi-like” endeavor focused more on attracting capital than generating revenue. To Colaiezzi, it was a genuine effort that came up short.

In multiple interviews with The Inquirer — granted, he said, against the advice of his attorney — Colaiezzi characterized the lawsuits as fallout from former partners who are jockeying for the last scraps of his assets. Those same investors, he said, did not object to his marketing campaign or salary decisions until the company went under.

Colaiezzi acknowledged making mistakes but denied that any of them amounted to fraud.

“I was always the first to admit I was not a tech executive,” he said. “I ran health clubs for a living. And I thought I was surrounding myself with the right people.”

His $6 million stock cash-out was one of those admitted mistakes. But he maintained it was a lawful transaction that took place three years before LifeBrand failed and was never concealed from investors.

The first investor lawsuit, filed in 2024, reached a settlement in March. Attorneys for the plaintiffs — among them former Eagles Brent Celek and Todd Herremans — declined to comment, citing a confidentiality agreement.

Meanwhile, a chorus of other backers who saw their capital vanish but have not taken Colaiezzi to court say that the CEO lured them with hollow promises and misled them about LifeBrand’s prospects long after the company began to collapse.

“I will never go as far as saying this should be on American Greed,” said investor John Cerasani, referring to the CNBC docuseries about white-collar criminals. “He’s not a con man. But it was 100% reckless behavior with other people’s money.”

From gym manager to tech CEO

The son of an IRS official and a homemaker, Colaiezzi went to Springfield High School, where he played lacrosse and built replicas of Victorian furniture. He became a volunteer firefighter, tried to open a deli, and dropped out of Pennsylvania State University before settling in the fitness industry.

He started cleaning gyms and ascended to regional manager, overseeing LA Fitness and Crunch Fitness locations. It was there, fielding complaints about things that personal trainers and other employees had posted online, that he got the idea for LifeBrand.

Colaiezzi saw a market full of people getting fired over old Facebook posts and pro athletes apologizing for the flippant tweets they made as teens. Companies wanted ways to vet prospective employees. The need for protection was urgent — a firewall against the damaging effects of a careless post lingering somewhere in the internet’s bottomless memory. Even the dating scene, riven by partisan politics, could benefit from an online cleanup.

After raising seed money from family and friends, Colaiezzi hired a Prague-based development company to build the software that made LifeBrand a reality.

His big break came in 2020, when he won a virtual pitch competition hosted by Kevin O’Leary from the hit show Shark Tank, who called Colaiezzi a “strong entrepreneur with every question answered.” The start-up won just $10,000 but earned something better than a cash prize: credibility.

Colaiezzi leveraged the pitch competition win into a Series A investor drive, securing over $27 million by the end of 2021, surpassing expectations.

He once told an interviewer that he wouldn’t sleep until he sold the company or until every investor was paid back. One financier, Nick Guiffre, a retired CEO of a manufacturing company, said he saw “the eye of the tiger” in Colaiezzi — a man who could make good on his word.

After losing more than half a million dollars in LifeBrand, Guiffre, who is not pursuing litigation, said he wished he had done more diligence.

“I don’t want to say I could afford to lose money,” he said, “but some people who put money in early on, it was their 401(k)s. It was their future.”

Colaiezzi filled out the top ranks of his company by hiring people he knew. LifeBrand’s earliest board members consisted of Colaiezzi, his brother, a doctor, and an early venture capital investor. His chief operating officer came from the fitness industry.

He maintains that they were qualified. But, like him, no one had real tech experience.

“I think I was too loyal to people who were with me from the beginning,” Colaiezzi said. “I should have operated it more like a competitive sports team, and not like a family.”

The shadow broker

Anthony Falco wanted everyone to know how excited he was about LifeBrand. Maybe too excited, his attorney would later concede in court.

“Dude, this LifeBrand thing is going to [be] f— HUGE,” he texted an investor in 2021. “Signed the Phillies yesterday! Big investors involved. You will thank your little Italian buddy for this someday very soon.”

Falco was a financial adviser and securities broker who worked at Central Pennsylvania-based Mid Penn Bank and Wayne-based Alden Investment Group. But he had a side job consulting for LifeBrand that involved hyping up its prospects to investors, according to the two lawsuits.

Gregarious and well-connected, he was Colaiezzi’s liaison to a world of high net-worth investors and sports influencers. Falco invited him to celebrity golf outings, introduced him to Mid Penn Bank’s CEO, and helped bring on big names like ex-Eagles Celek and Herremans.

“We were banking at TD Bank at one point, and then [Falco] invited me golfing with the CEO of Mid Penn Bank,” Colaiezzi said. “And, you know, why wouldn’t you want to bank with a smaller bank where you got the CEO’s phone number?”

To Colaiezzi, sports were LifeBrand’s ticket to fame.

Between 2021 and 2023, LifeBrand paid millions to the Eagles, Phillies, and Sixers in a deal that included naming rights for a gate at Lincoln Financial Field and access to the Eagles Tunnel Club, a 1,400-square-foot lounge where VIPs could rub shoulders with the home team’s players as they hit the field.

Investors contend both Falco and Colaiezzi deceptively cast these deals as investor partnerships, rather than paid campaigns. According to the lawsuit initiated by the group that included Celek and Herremans, Falco received over a million shares of LifeBrand stock for inducing investors to the company through exaggerated claims, despite telling one that he was not allowed to accept comped shares.

While working out of LifeBrand’s offices, he texted investors that LifeBrand was going to be “a billion dollar company,” hyping up talks with the NFL and Jay-Z’s Roc Nation. In another text, Falco said LifeBrand was projected to make $58 million in revenue in 2022. But he also cautioned the investor that “nothing is real UNTIL we see that it is real!!”

LifeBrand’s revenue at the end of that year: $496,005.

In a motion to dismiss the 2024 lawsuit, Falco’s attorney Sean Bellew wrote that his client was at most guilty of being “overly enthusiastic” about LifeBrand and denied misleading anyone.

Both Mid Penn and Alden, which investors in that case accused of failing to supervise Falco, denied wrongdoing. Mid Penn argued in court that it had no formal relationship with the investors and that Falco’s work for LifeBrand was an outside matter. The bank declined to comment, citing pending litigation.

Alden argued much of Falco’s work at LifeBrand occurred prior to his joining the firm, which never formally advised any of the investors. Alden nonetheless paid $500,000 in March through its insurance policy to settle the 2024 lawsuit, according to Falco’s FINRA broker check page. The firm did not respond to a request for comment.

As for the new lawsuit, Bellew told The Inquirer that Falco never met the plaintiffs who renewed the allegations against him. Falco, he said, was “a victim” of Colaiezzi’s characterizations about the company — same as the other investors.

The Hail Mary marketing plan

For a self-made CEO from Delco, seeing his company’s name lit up across three stadiums was glorious. It was also a gamble for a young, unprofitable company. Last year, for example, the Tunnel Club naming rights were acquired by Janney Montgomery Scott, a wealth management and investment advisory firm with more than 100 offices and $1 billion in yearly sales.

Colaiezzi said he told investors about a third of the start-up capital would go toward marketing and said the stadium blitz had their support at the time. He produced text messages from investors who later sued him, which showed them asking for access to VIP seats and praising the buzzy brand campaign.

“There’s not a single email, text, or phone call with any adviser or board member saying ‘you shouldn’t be spending money on this,’” Colaiezzi said. “Everyone was in line until we ran out of money.”

Between 2021 and 2023, records show, LifeBrand spent over $16 million on advertising and marketing contracts — more than half its venture-capital haul.

Colaiezzi said the marketing helped introduce customers to LifeBrand, which scanned millions and deleted tens of thousands of social media posts over those years. He said his sales team used the stadiums to pursue multimillion-dollar contracts with major institutions and companies.

Some investors told The Inquirer they always had doubts about the marketing. Cerasani, a venture capitalist and gambling influencer, had been wooed as a potential investor with sideline tickets and access to the Tunnel Club, with its open bar with premium liquors, and a buffet with shrimp cocktail and prime rib.

Every time Cerasani visited, he said, it looked like a private party for LifeBrand executives and Colaiezzi’s close friends, who treated him like “a king.” Rarely did he see prospective clients.

Colaiezzi denied that characterization. But the gap between the marketing spend and the revenue it produced was impossible to ignore. By 2023, the company was losing over $800,000 a month, according to internal financial records reviewed by The Inquirer.

Sales reps would take clients to games and work them for months to close a modest $12,000 sale, Colaiezzi acknowledged. The big institutional contracts were not coming through.

Yet he kept sending optimistic signals to investors.

In an August 2023 email obtained by The Inquirer, Colaiezzi announced that he had just closed a “transformative deal” with a Denver-based education nonprofit — a three-year, $63 million contract that would use LifeBrand’s data to help students at underserved schools.

It is not clear how the client, which has no online presence and no publicly available nonprofit filings, was equipped for a deal of that size. The revenue never materialized, and one investor alleged in court that the deal was fiction.

Colaiezzi said the eight-figure contract was real. He assigned two full-time employees and flew out to meet with leaders, but the nonprofit backed down before the bills were due. If anything, Colaiezzi said, “we got scammed by them.”

Bedlam in the bank

In May 2024, a group of anxious investors gathered on a video call to discuss the millions they’d sunk into LifeBrand.

The company was on the brink of collapse. The money was gone. And all that the investors had to show for their backing were memories from the Eagles VIP suite.

As they raised concerns on the call, one investor shared that Colaiezzi had paid himself a $6.17 million stock redemption at a time when the company had little revenue, according to four people who attended the meeting. Outrage erupted.

“It was very obvious that things were going off the rails,” said Dan Ellison, a business owner who had invested in the start-up with his wife. “But no one knew that [Colaiezzi] took $6 million.”

According to Colaiezzi, the 2021 stock redemption was done at the urging of shareholders at the time to dilute his control in the company, and was documented on capitalization tables shared with subsequent investors.

He said he put $3 million back into the start-up to keep it afloat as he pursued a Series B fundraising round that would generate an additional $50 million — money that could finally turn LifeBrand profitable. That never happened.

Inside LifeBrand’s offices in West Chester, uncertainty spread.

Simon Wong, an engineer who worked at LifeBrand for a year until he was laid off in May 2024, recalled a workplace without the start-up grind culture. Most employees left each day at 4 p.m., and at 2 p.m. on Fridays, he said. Wong said he believed in the product and saw Colaiezzi as a leader who cared and said “the right things” about his mission.

By May, Wong said, software subscriptions stopped getting paid and paychecks were late — then they stopped entirely.

Colaiezzi agreed to fire himself as CEO, along with his other longtime executives. Then the rest of the board quit, leaving only Colaiezzi to run the company. He begged investors for patience while working with an outside firm to stave off bankruptcy. He laid off the entire staff and then tried to bring some of them back for a slimmed-down version of LifeBrand.

“It kind of felt like we were getting strung along,” said Wong, who said he is still owed pay from most of his final month working at the start-up.

LifeBrand — which Colaiezzi valued at $137 million in 2021 — was sold in August 2024 for $75,000 to Sentiment AI, an acquisition company formed by AI consultancy Global Fusion. Colaiezzi was initially kept on as an adviser, but the future of the company would be in the hands of more seasoned tech leaders. He said most investors agreed to convert their shares into the new venture in exchange for a promise not to sue.

Another group of investors took him to court. And the company’s turnaround effort stalled almost immediately, which Colaiezzi blamed on the litigation.

“It hit a point where people wanted to kind of run or protect themselves,” Colaiezzi said.

‘It’s like I lost my baby’

One day last month, inside the restored 19th-century workshop in West Chester where LifeBrand operated for years, Colaiezzi walked solemnly past whiteboards crowded with years-old strategy notes. Framed Eagles, Sixers, and Phillies jerseys still hung on the wall.

He said in an interview that he feels “a weird obligation” to come to the office every day, while it is still his.

The building, which Colaiezzi purchased for $2.7 million with other investors and leased back to LifeBrand, is under foreclosure. Now he sat alone at a folding table among packed boxes in what used to be a conference room.

“It’s like I lost my baby, you know?” he said. “There was so much great potential.”

Moving on involves finalizing the lawsuits and paying off debt. Lenders and investors have placed liens on Colaiezzi’s Jersey Shore home. Asked if he got in over his head, Colaiezzi said, “Yeah, probably.”

But he is making plans to erase the LifeBrand failure and replace it with a success story.

His next venture, he said, is “a family-first social network” powered by AI.

Parents will be able to upload family histories, recipes, and advice for their children. The idea, he explained, is that children living in a harsh world should be able to get answers to sensitive questions from their own families rather than a remote server.

“The AI will basically learn how Grandpop would answer a question,” he said, “not how ChatGPT would.”

The pitch has already secured $50,000 from investors.

Staff writers Joseph DiStefano, Samantha Melamed, and Abraham Gutman contributed to this article.

The Inquirer’s journalism is supported, in part, by the Lenfest Institute for Journalism and readers like you. News and editorial content are created independently of The Inquirer’s donors. Gifts to support The Inquirer’s high-impact journalism can be made at inquirer.com/donate. A list of Lenfest Institute donors can be found at lenfestinstitute.org/supporters.