Brokers feeling subprime squeeze

With Wall Street rattled and lawmakers taking notice, risky loans are drying up.

Ricky Boone is a Trevose mortgage broker whose customers typically have poor credit, many of them seeking loans for 100 percent of the value of their property.

The so-called "subprime-mortgage" scare changed all that.

A borrower with a credit score of 580 - on a scale of 400 to 800 - can no longer get 100 percent financing, he said.

"Nobody will buy it," he said of the investors that used to buy such subprime loans from mortgage companies. "People now looking to buy houses, they are going to have to have more down-payment money," said Boone, president of Excel Capital Funding Inc.

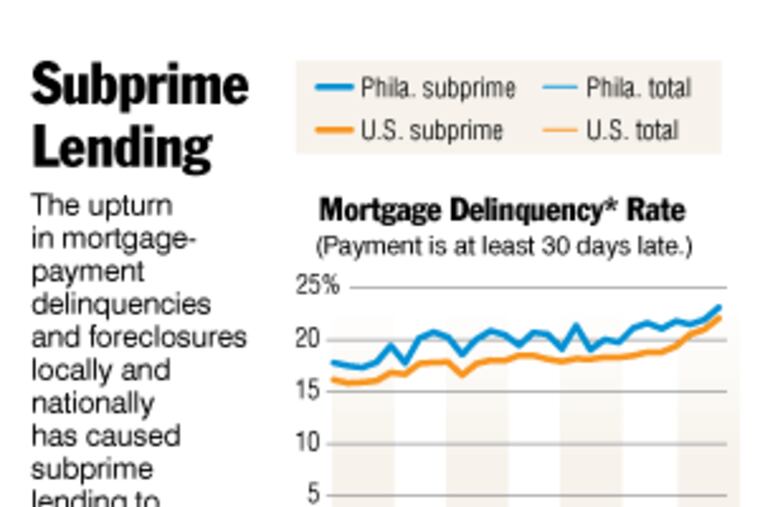

So far, the scare has been limited to the subprime market, which includes people with credit scores of about 620 and lower. That market represented about 19 percent of the overall mortgage business a year ago, but it is projected to fall 30 percent this year, according to the Mortgage Bankers Association.

That is squeezing subprime brokers such as Boone.

Wall Street's concern moved from simmer to boil after a major subprime lender, New Century Financial Corp., warned this month that it would not make new loans, because its bankers had cut off credit. Investors worried that more lenders would fail, with subprime borrowers falling behind on their mortgages in the fourth quarter at the highest rate in four years.

Even though three lenders Boone was using have shut down, and others are changing their guidelines every day, Boone said he did not buy into the fear that the subprime market was going away.

"They are tightening up right now, and it's going to be like that for six or eight months. Then it will come back. It always does," said Boone, who has been in the mortgage business for 18 years.

Most mortgages are sold by the original lender and incorporated into securities bought by pension funds and other investors. Demand for such securities has plummeted with rising default rates.

Moody's Investors Service, the debt-rating agency, said yesterday that it would change the way it rates bonds backed by the riskiest mortgages.

For now, worry that the subprime rattles will spread into the broader mortgage market is keeping Wall Street on edge and rousing lawmakers in Washington.

Today, the Senate Banking Committee is scheduled to hold a hearing on the collapse of the subprime market and its potential consequences. Among those scheduled to testify is Philadelphia consumer lawyer Irv Ackelsberg, who has been a longtime critic of the subprime industry.

"Most of the loans are made to existing homeowners who are being essentially fooled into consolidating their credit cards into one of these ridiculous mortgages," such as a $10,000 home repair wrapped up in a $45,000 loan, said Ackelsberg of Langer & Grogan P.C., of Center City.

Lenders were racing to keep the mortgage and housing boom going with new sorts of mortgages, such as interest-only loans, loans with payments that did not even cover interest, and so-called "stated-income" loans, for which borrowers did not even need a job.

"You would see month after month, quarter after quarter, these subprime-mortgage companies getting more and more aggressive," said Michael Dougherty, a managing member of Choice Mortgage L.L.C., of Mount Laurel.

That strategy helped U.S. mortgage debt double over the last five years to $8.2 trillion, according to Moody's Economy.com in West Chester.

As long as housing prices kept going up, lenders were willing to take on more risk, because the borrower could always refinance based on a higher appraisal, or, if it came to foreclosure, the increased value of the house would cover foreclosure costs.

That game is up now that housing prices have flattened out. "The unraveling will occur over the next year," said Mark Zandi, chief economist at Moody's Economy.com.

As many consumers are shut out of treating their houses like giant ATMs, economic growth will be slower than it would have been otherwise. "I think a lot of people will decide they don't need granite countertops," said David Wyss, chief economist at Standard & Poor's.

For now, brokers, described by some as the street-level sales force for Wall Street banks, are scrambling for new business and struggling to finish up some old business.

"There's nothing left. It all disappeared in a heartbeat," said Bill Metalsky, a loan officer with Creative Mortgage Group Inc., of Willow Grove, which had 15 percent to 20 percent of its business in the subprime arena.

Metalsky said he had a customer with a very low credit score, but a 20 percent down payment. It would have been easy to find a lender at the beginning of the year. "Now I can't find anybody. Now I would have to have 40" percent down, he said.