Will Philly lawyer Uchimoto's case boost U.S.-style corporate governance in Japan?

The company's condominium, real estate and legal departments were fooled by a broker who convinced them to buy the property even though his client "was not the owner,"

Sekisui House is an Osaka, Japan-based home builder. Sort of a Pacific Toll Bros., with branches in the United States and Australia.

The $2.2 billion (in yearly sales) company's share price has recovered with Japan's economy over the last decade, but has trailed the Nikkei average in recent weeks, after a split in its governing board led to the departure of chairman Isami Wada. He had been with the company since 1965, soon after its founding.

Sekisui said Wada left voluntarily. But Wada, in a series of statements, has disputed that. He says he was forced out improperly by board members and managers in defiance of a personnel committee recommendation that would have kept him in place and instead removed senior managers he says are responsible for an embarrassing $51 million loss on a fraudulent land deal. He wants them replaced and his reputation cleared.

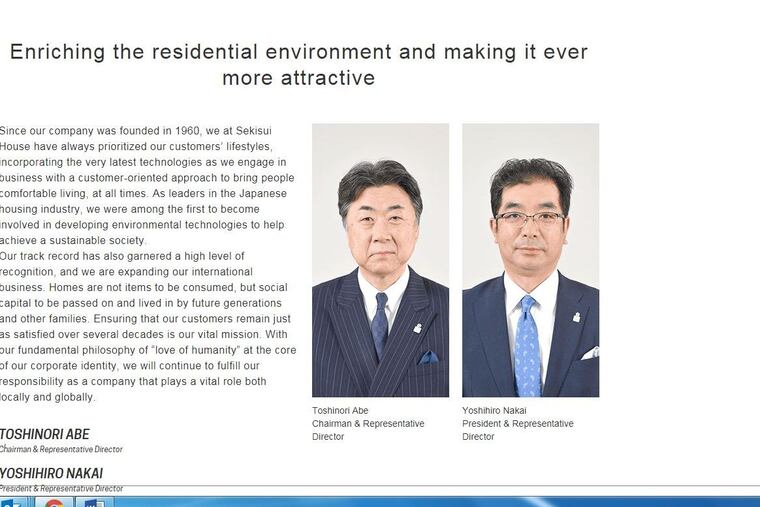

Sekisui's current leaders — former president Toshinori Abe, who replaced Wada as chairman; vice chairman Shiro Inagaki; and current president Yoshihiro Nakai — say Wada retired voluntarily due to his age (76).

In the U.S., this sounds like a fight for the fast-moving, business-friendly Chancery Court in Delaware, where more than half of New York Stock Exchange firms are legally based. Or grist for class-action shareholders' lawsuits. Or maybe a call for a quick disclosure demand from the Securities and Exchange Commission detailing who in senior management was most responsible for the loss.

Japanese securities regulators have not seen fit to move publicly at this time. That puts the onus to act on investors, who must vote on the board, now dominated by Abe and his allies, on April 26.

But in the globalized stock market, many of Sekisui's owners are also here in the U.S. So Wada's legal counsel, Makoto Saito, has hired Philadelphia-based attorney William Uchimoto, a Japanese American who was general counsel at the former Philadelphia Stock Exchange and has represented investors in many disputes.

Uchimoto has approached the Institutional Shareholder Service and Glass-Lewis proxy services, which advise investors on corporate governance issues, hoping that big U.S. shareholders like BlackRock and Vanguard Group will study the controversy and vote in an informed way at Sekisui's annual meeting April 26. Officials at ISS and Glass-Lewis tell me they may make recommendations on the case in early April.

This multinational corporate drama follows Sekisui House's costly aborted purchase of a 23,000-square-foot property near Tokyo's Gotanda commuter rail station. A summary report that the company released March 6 blames failures by the firm's operating departments.

The company's condominium, real estate, and legal departments were fooled by a broker who persuaded them to buy the property even though his client was not the owner, according to the company announcement detailing the fraud.

There were warnings, to be sure. Multiple departments of Sekisui had "received multiple pieces of risk information concerning the transaction," according to the report. The warnings piled up "by visit, telephone, written notice, and other means."

But Sekisui managers brushed all that aside: They "considered the said risk information to be a type of harassment" to slow the deal. They were confident whoever was trying to kill the sale would stop once they got title.

That didn't happen. The warnings turned out to be accurate. Authorities refused to give Sekisui title to a property they said the supposed seller didn't own, and Sekisui lost $51 million. The loss was reported to police, who have been investigating.

In its failure analysis, Sekisui found "the specifics of the transaction should have been more carefully and thoroughly examined" by people close to the deal. The managing officers of the condominium, legal and real estate departments accordingly resigned. The investigation at points appears to absolve higher management, noting "it is very difficult for the head offices" to flag fraudulent land brokers.

But the report also noted that company directors should accept general responsibility for the consequences, and top officers had an "ethical responsibility."

Wada says there was more. In a written statement, he said a company investigation by the independent board members last year found — in a detailed report that hasn't been released — that Abe "moved recklessly fast and refused to see red flags that the land seller was a fraudster." Wada said the personnel committee of auditors and mostly independent directors initially "voted 5-0 to remove Abe as president." And on Jan. 24, chairman Wada took that recommendation to the full board.

But Abe pushed back. In its first poll, the board deadlocked 5-5, with outsiders endorsing the committee recommendation but insider directors voting to keep Abe, Wada said. By the end of the meeting, enough directors had switched to giving Wada's job as chairman to Abe, while keeping Wada as an adviser. The company says Wada agreed to step down as president, which Wada denies. He has urged the company to make public the full committee report. And he wants Abe and his allies out.

"As a U.S. securities attorney, I see this story as an interesting one to compare with what would be happening if Sekisui was a U.S.-listed company on Nasdaq or the New York Stock Exchange," Uchimoto told me. "The SEC would be all over this for disclosure failures," and the entire investigation report could be disclosed as material information in a Form 8-K filing by now.

Sekisui management is standing firm in favor of Abe's team. But Uchimoto hopes to set a precedent: "Japanese corporate governance has a long way to go for a major public company, and this may be the case that creates some positive changes."

(added April 2): Among the lawyers and governance-watchers looking at the Sekisui House case is Merritt Cole, counsel at Earp Cohn in P.C. Like Uchimoto, Cole is a past SEC staff lawyer; the two co-taught a Securities Regulation course at Drexel Law School. According to Cole, the public record suggests "a number of breakdowns in corporate governance at Sekisui House, including a lack of mechanisms to identify and communicate risks in business transactions to the Board and to insure that investors receive accurate and timely information." He expects the gaps in the accounts of Wada's replacement by Abe might be "very troubling to U.S. shareholders" — and that independent legal counsel to improve both internal procedures and external compliance could address resulting reputation concerns.