Beneficial Bequest

With a net worth approaching $25 million, Ridgely "Ridge" Bolgiano this year left his alma mater, Haverford College, a $6.5 million gift using a relatively obscure form of retirement savings and philanthropy that benefits both the charity and the donor while he's still living.

With a net worth approaching $25 million, Ridgely "Ridge" Bolgiano this year left his alma mater, Haverford College, a $6.5 million gift using a relatively obscure form of retirement savings and philanthropy that benefits both the charity and the donor while he's still living.

The vehicle in question - a charitable gift annuity - increased both Bolgiano's retirement income and the amount he left the college.

And they aren't just for the wealthy - the rest of us can use them, too.

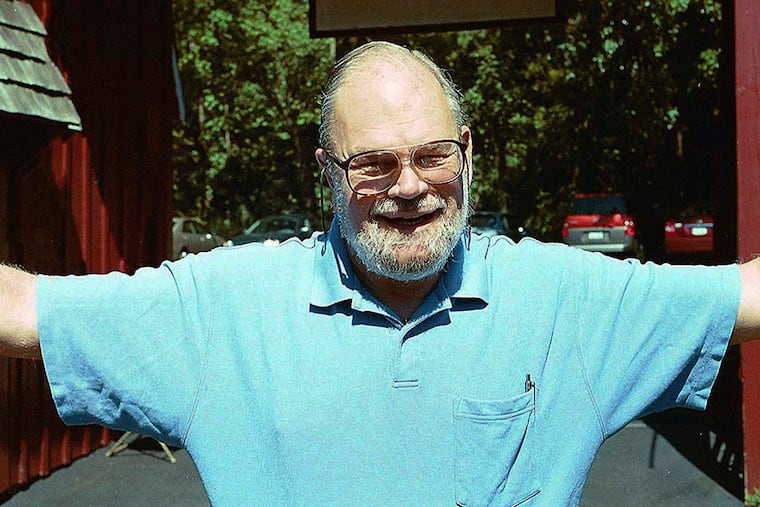

Bolgiano graduated from Haverford in 1959 and, until his death at age 82 on Oct. 3, he lived in Gladwyne. A confirmed bachelor, he had no spouse or children.

He was an inventor and technology millionaire who made his fortune with InterDigital in King of Prussia; he was a physicist who owned more than two dozen patents, one of which is central to our everyday lives, the means by which a cellphone signal is transferred from cell to cell in a service provider's network.

As he approached retirement, Bolgiano set up a "deferred" charitable gift annuity.

Such annuities are relatively unknown because banks, stockbrokers and financial planners don't sell them. Only 501(c)(3) charitable organizations can offer them, according to Chris Mills, a spokesman for Haverford College.

Eileen Heisman, president and CEO of the National Philanthropic Trust, calls charitable gift annuities "great giving vehicles."

They are complex on the inside, but fairly easy to set up.

A charitable gift annuity is a contract between you and a university, religious entity, hospital, or other charity. You can fund one with a gift of just $10,000 in some cases.

The benefits: Your annuity payments may be treated as partly tax-free income. You receive an immediate charitable tax deduction for a portion of your gift. And if you fund your charitable gift annuity with appreciated securities, there are no up front capital gains taxes.

Steven Kavanaugh, director of gift planning at Haverford College, explains that donors get an Individual Retirement Account-style tax break when they fund the gift annuity, and income plus partial return of principal from the start date they specify until their death. At that point, the rest passes to the charity.

In Bolgiano's case, Haverford was the lucky charity.

"You can never outlive this type of annuity because the charity is obligated by law to make the income payments to you until your death," Kavanaugh says.

A portion of future income payments are tax-free (typically about 25 percent).

"These also work for middle-class people because a donor can fund one at a modest level and get the same benefits," Kavanaugh says.

How they work

Transfer cash or securities to your favorite charity. That charity then pays you a fixed income for the remainder of your life. What's left passes to the charity when you die.

How much will you earn annually?

That's the key. The charitable gift annuity rate is based on your age.

The older you are, the greater your payment. Annuity rates are based on guidelines established by the American Council on Gift Annuities, and they change often. For updated payout rates, visit www.acga-web.org.

Unlike IRAs, which are subject to rules about payouts and drawdowns, you can choose the age at which you would like your payout to begin.

Bolgiano's annuity was a special case.

At age 70, he funded the annuity with $500,000 but deferred the income payments until he reached age 78.

His delay resulted in the annuity compounding for years.

"When he finally did initiate the payout, both the amount he got and the amount available to Haverford upon his death were much greater," Mills says.

Because Bolgiano deferred payments, he got a higher current tax deduction and a rate of return of about 8 percent, Kavanaugh says. In the year he made the gift, Bolgiano's tax deduction totaled just over $279,000.

Had he started to receive the payments immediately, returns would have been about 5 percent annually, with a deduction of $195,000.

"It's a good option for people who have charitable intent. Whether you fund at $25,000 or more, the reality is you are better off financially if you just go out to the marketplace and buy a commercial annuity, not a charitable annuity," Kavanaugh says.

"But what this arrangement does, however, is if you have some charity you love, it allows you to make a charitable gift that costs you less money."

215-854-2808@erinarvedlund