Campbell Soup Co. buying snack company Snyder's-Lance for $4.9 billion

In its biggest acquisition ever, Campbell Soup Co. said it will pay $4.87 billion for snack maker Snyder's-Lance Inc., whose brands also include Kettle and Cape Cod potato chips, in a bid for the revenue growth that has eluded the Camden company for years.

In its biggest acquisition ever, Campbell Soup Co. said Monday that it would pay $4.87 billion for snack maker Snyder's-Lance Inc., whose brands also include Kettle and Cape Cod potato chips — a bid for the revenue growth that has eluded the Camden company for years.

The deal, Campbell's sixth in the last five years, stands in sharp contrast to most of its other recent acquisitions. Those were designed to move Campbell into fresher-food categories seen by its leadership as more in line with today's consumers, though management frequently highlighted snacks as a target for expansion.

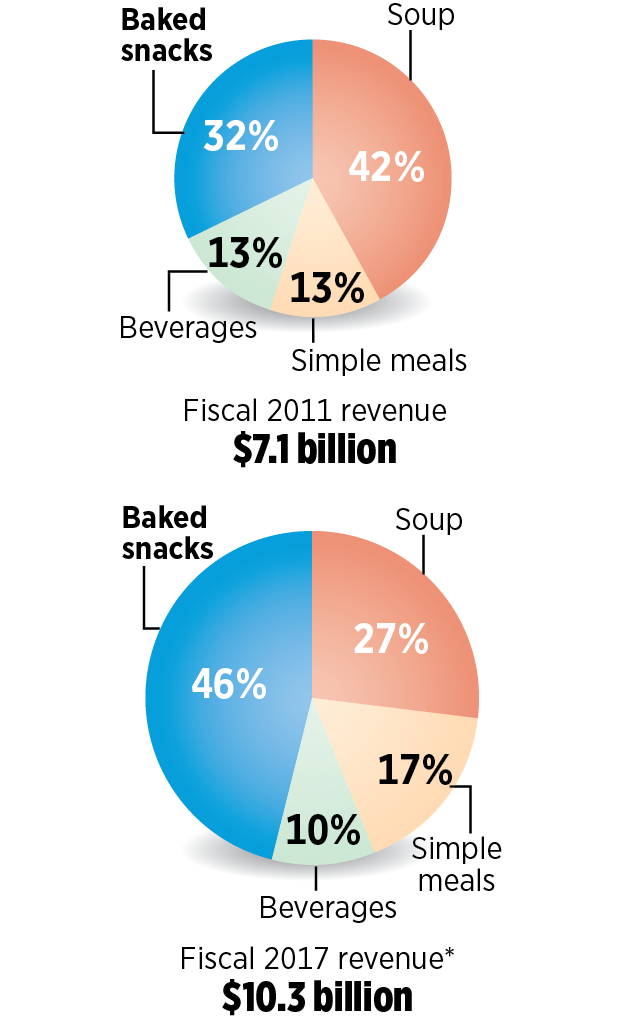

"With the addition of Snyder's-Lance to Campbell, we will dramatically shift our portfolio toward the faster-growing snacking category," Campbell's president and chief executive, Denise Morrison, told analysts on a conference call. Snacks will amount to nearly half of Campbell's annual revenue, while soup will fall to slightly more than a quarter.

"This is a truly remarkable transformation for Campbell, and I'm confident that it will lead to an improved growth profile," Morrison said.

With the addition of Snyder's-Lance, Campbell's annual revenues are expected to exceed $10 billion, a five-year goal Morrison set in 2014.

Luca Mignini, president of Campbell's global biscuits and snacks unit, which will include the newly acquired brands, said Snyder's-Lance has had 4 percent annual revenue growth in recent years, excluding acquisitions — far better than Campbell overall, which has struggled to increase revenue.

Four percent is not bad, said Mitchell B. Pinheiro, who works in portfolio management and research at Costello Asset Management Inc. in Feasterville and has followed Campbell for many years.

"In food, flat is the new up," Pinheiro said.

Campbell’s Shifting Business

"Campbell's is aggressively trying to reshape their portfolio into growth categories and growth channels, and this helps them do it," he said of the Snyder's-Lance acquisition. It's a plus that Snyder's-Lance fits with Pepperidge Farm, the crown jewel of the Campbell portfolio, because that gives it a better chance of success, he noted.

There are risks to the deal, though. "It's not a layup, this acquisition," and it takes Campbell out of future deals because it is going deep into debt to pay for it, Pinheiro said.

Without prompting, both Morrison and Mignini emphasized that Snyder's-Lance occupies familiar territory.

"We know snacking," Mignini said."Pepperidge Farm has been performing fantastically well, if you look at the performance of Goldfish, Milano, biscuits in general."

By contrast, Campbell has had a hard time making a success of Bolthouse Farms Ltd., which it bought for $1.55 billion in 2012. Bolthouse sells fresh carrots, but it was most attractive for its refrigerated beverages and is the cornerstone of the company's Campbell Fresh unit.

Campbell agreed to pay $50 per share for Snyder's-Lance. That represents a 27 percent premium over Snyder's-Lance's closing price on Dec. 13, the last day before the first reports that Campbell was trying to buy the Charlotte, N.C., snack company, which was the result of the 2010 merger of Lance Inc. and Pennsylvania-based Snyder's of Hanover Inc.

Campbell's shares rose slightly Monday, up 0.07, or 0.14 percent, to close at $49.66. Shares of Snyder's-Lance rose 3.25, or 6.95 percent, to close at $50.04.

The deal requires the approval of Snyder's-Lance shareholders. Closing is expected in the spring.

The total price, including the assumption of debt, is about $6.1 billion, according to Standard & Poor's, which downgraded Campbell's credit rating by one notch, to BBB from BBB-plus, and gave the company a negative credit outlook.

The credit downgrade reflects "the inherent integration risks of such a large acquisition, and the risk that Campbell's Fresh segment will continue to underperform, as well as that Snyder's-Lance relatively weak margins may not rebound, thus causing Campbell to struggle to reduce leverage" over the next two years, S&P said.

At the same time, S&P said, Campbell needs to reverse negative trends in its Campbell Fresh division, improve the margins of the Pacific Foods business it bought for $700 million this month, and contend with the ongoing decline in its high-margin soup business.

By its own admission, Snyder's-Lance has been a laggard in translating sale growth in terms of profits, with its adjusted operating profit margin of 8.8 percent ranking near the bottom in a group of 16 unnamed peers last year, according to a September investor presentation. The average for the group was 16 percent.

Snyder's-Lance also significantly underutilized about half of its manufacturing facilities, the presentation said.

"Lance has been a perennial underperformer, perennial. I've covered them for years," Pinheiro said.

Campbell sees opportunity. "When we look at the structure of Snyder's-Lance, we can definitely leverage a lot of the know-how we have in critical functions like logistics, manufacturing, procurement" to make the newly acquired company significantly more profitable, said Mignini, the Campbell executive who will oversee Snyder's-Lance.

Despite its troubles, Snyder's-Lance has a big market presence. Snyder's of Hanover pretzels and Lance sandwich crackers are the best-selling brands nationally in their categories, according to Campbell. Combined, Cape Cod and Kettle chips are the best-selling kettle-style chips. Additional Snyder's-Lance brands include Pretzel Crisps, Late July organic/natural tortilla chips, Pop Secret microwave popcorn, and Emerald nuts.

"I do believe that there are significant opportunities there," Mignini said.